Crypto tax is something every cryptocurrency investor must understand. If you buy, sell, trade, or earn digital coins like Bitcoin or Ethereum, you may owe crypto tax. Many beginners think crypto is anonymous and tax-free. However, that is not true. Governments across the world now treat cryptocurrency as taxable property or income.

- What Is Crypto Tax?

- Why Governments Tax Cryptocurrency

- When Do You Owe Crypto Tax?

- Capital Gains Tax on Cryptocurrency

- Income Tax and Cryptocurrency

- How to Calculate Crypto Tax Step by Step

- Step 1: Track All Transactions

- Step 2: Calculate Cost Basis

- Step 3: Calculate Profit or Loss

- Step 4: Apply Tax Rate

- Common Crypto Tax Mistakes Beginners Make

- 1. Not Reporting Small Trades

- 2. Forgetting Crypto-to-Crypto Trades

- 3. Ignoring Staking Rewards

- 4. Poor Record Keeping

- 5. Assuming Exchanges Report Everything

- Crypto Tax Around the World

- Visual Guide: How Crypto Tax Works

- How to Reduce Your Crypto Tax Legally

- 1. Hold Long-Term

- 2. Offset Losses

- 3. Use Tax-Loss Harvesting

- 4. Keep Detailed Records

- 5. Consult a Tax Professional

- Do You Pay Crypto Tax If You Lose Money?

- What Happens If You Don’t Report Crypto Tax?

- The Future of Crypto Tax

- Frequently Asked Questions (FAQs)

- 1. Do I pay crypto tax if I only buy and hold?

- 2. Is transferring crypto between wallets taxable?

- 3. Do I pay crypto tax on gifts?

- 4. How do tax authorities track crypto?

- 5. Can I avoid crypto tax?

- 6. Are NFTs taxed like crypto?

- 7. Do I need special software for crypto tax?

- Final Thoughts on Crypto Tax

So, what exactly is crypto tax? How does it work? When do you need to pay it? And how can you calculate it correctly?

In this complete beginner’s guide, you will learn everything about crypto tax in simple and clear language. Whether you are new to crypto or already investing, this guide will help you stay informed and avoid costly mistakes.

What Is Crypto Tax?

Crypto tax refers to the taxes you must pay on profits earned from cryptocurrency transactions. Most tax authorities treat crypto as property or a digital asset, not as regular money.

That means when you sell or trade crypto and make a profit, you may need to pay capital gains tax. If you earn crypto from mining, staking, or as payment, you may need to pay income tax.

In simple words:

- Profit from selling crypto = Capital gains tax

- Earning crypto as income = Income tax

Different countries have different rules. For example, in the United States, the Internal Revenue Service (IRS) requires taxpayers to report cryptocurrency transactions.

You can always stay updated with the latest crypto tax news and updates on platforms like https://www.cryptonews21.com and refer to official guidelines such as the IRS crypto tax page here: https://www.irs.gov/businesses/small-businesses-self-employed/digital-assets

Why Governments Tax Cryptocurrency

At first, many people believed cryptocurrency was beyond government control. However, as crypto became popular, governments stepped in.

There are three main reasons:

1. Revenue Collection

Governments collect taxes to fund schools, hospitals, roads, and public services. Crypto profits are treated like stock or real estate profits.

2. Financial Transparency

Tax reporting helps prevent illegal activities like money laundering.

3. Investor Protection

Clear tax rules create a safer environment for investors.

As crypto adoption grows, crypto tax rules become stricter and more defined.

When Do You Owe Crypto Tax?

Not every crypto activity triggers crypto tax. However, many common actions do.

Here is a simple table to help you understand:

| Crypto Activity | Is It Taxable? | Type of Tax |

|---|---|---|

| Buying crypto with cash | No | None |

| Selling crypto for profit | Yes | Capital Gains |

| Trading one crypto for another | Yes | Capital Gains |

| Using crypto to buy goods | Yes | Capital Gains |

| Receiving crypto as salary | Yes | Income Tax |

| Mining rewards | Yes | Income Tax |

| Staking rewards | Yes | Income Tax |

| Receiving crypto as a gift | Usually No (for receiver) | Depends on country |

If you only buy and hold crypto, you generally do not owe crypto tax until you sell.

Capital Gains Tax on Cryptocurrency

Capital gains tax applies when you sell crypto for more than you paid for it.

Let’s look at a simple example:

- You buy Bitcoin for $1,000.

- You sell it later for $1,500.

- Your profit is $500.

- That $500 is taxable.

Short-Term vs Long-Term Gains

Most countries divide capital gains into two types:

| Type | Holding Period | Tax Rate |

|---|---|---|

| Short-term | Less than 1 year | Higher rate |

| Long-term | More than 1 year | Lower rate |

Holding your crypto longer may reduce your crypto tax bill.

Income Tax and Cryptocurrency

Not all crypto profits come from selling.

You may earn crypto in several ways:

- Mining

- Staking

- Getting paid in crypto

- Airdrops

- Referral rewards

When you receive crypto as income, the value at the time you receive it is taxed as ordinary income.

Later, if you sell that crypto and make a profit, you also pay capital gains tax on the extra profit.

Yes, this means crypto tax can apply twice in some cases.

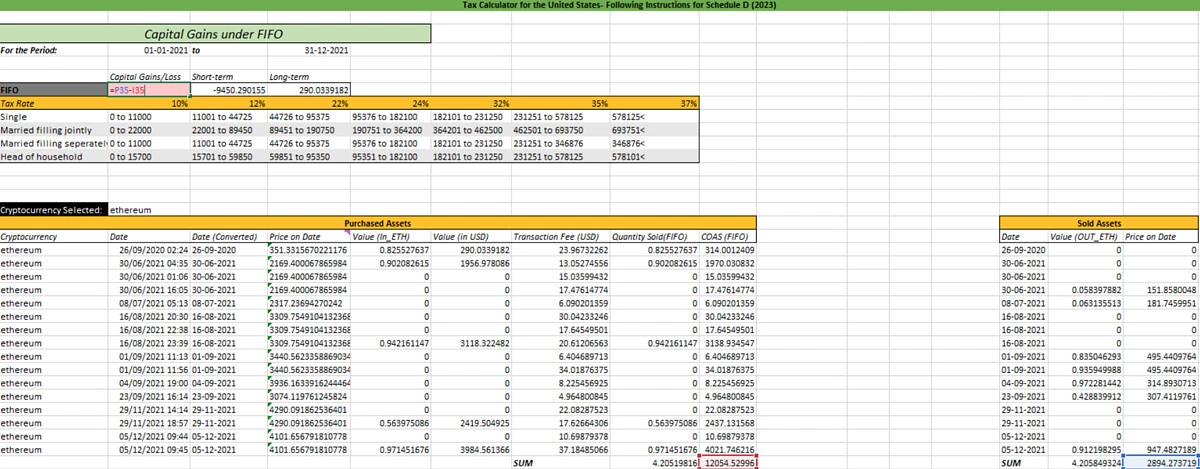

How to Calculate Crypto Tax Step by Step

Calculating crypto tax may seem difficult at first. However, you can break it down into simple steps.

Step 1: Track All Transactions

Keep records of:

- Date of purchase

- Purchase price

- Date of sale

- Sale price

- Transaction fees

Step 2: Calculate Cost Basis

Cost basis = Purchase price + fees.

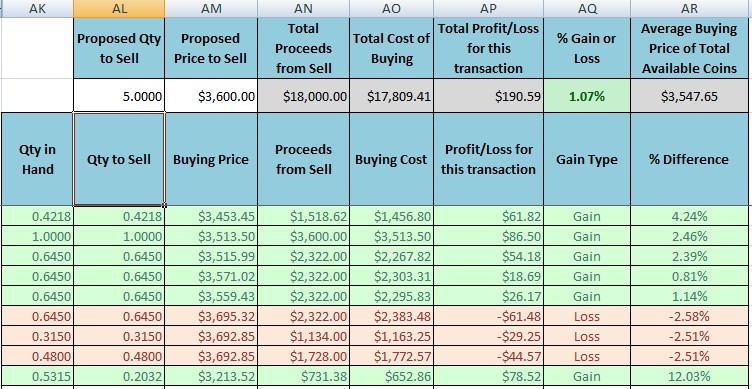

Step 3: Calculate Profit or Loss

Profit = Sale price – Cost basis.

Step 4: Apply Tax Rate

Apply the correct capital gains or income tax rate based on your country.

Here is a basic formula:

Taxable Gain = Selling Price – (Purchase Price + Fees)

Using crypto tax software can help automate this process.

Common Crypto Tax Mistakes Beginners Make

Many new investors make costly errors. Avoid these mistakes:

1. Not Reporting Small Trades

Even small crypto trades can trigger crypto tax.

2. Forgetting Crypto-to-Crypto Trades

Trading Bitcoin for Ethereum is taxable in many countries.

3. Ignoring Staking Rewards

Staking income is often taxable.

4. Poor Record Keeping

Without records, you may overpay or underpay taxes.

5. Assuming Exchanges Report Everything

Not all exchanges report to tax authorities.

Keeping detailed records helps you stay safe and stress-free.

Crypto Tax Around the World

Crypto tax rules vary by country.

Here is a simplified comparison:

| Country | Crypto Treated As | Capital Gains Tax | Income Tax |

|---|---|---|---|

| USA | Property | Yes | Yes |

| UK | Property | Yes | Yes |

| Germany | Private Asset | No (if held 1+ year) | Yes |

| Canada | Commodity | Yes | Yes |

| Australia | Property | Yes | Yes |

Always check your country’s official tax authority website.

Visual Guide: How Crypto Tax Works

These visuals show how crypto tax applies when you buy, sell, trade, or earn cryptocurrency.

How to Reduce Your Crypto Tax Legally

Nobody wants to pay more tax than necessary. Here are legal ways to reduce your crypto tax:

1. Hold Long-Term

Long-term gains often have lower tax rates.

2. Offset Losses

If you lose money on some trades, you may offset gains.

3. Use Tax-Loss Harvesting

Sell losing assets before year-end to reduce taxable gains.

4. Keep Detailed Records

Accurate records prevent overpayment.

5. Consult a Tax Professional

Crypto tax laws can be complex.

Never try to hide crypto profits. That can lead to penalties.

Do You Pay Crypto Tax If You Lose Money?

If you sell crypto at a loss, you usually do not owe crypto tax. In fact, losses may reduce your overall tax bill.

Example:

- Gain from Bitcoin: $1,000

- Loss from Ethereum: $600

- Taxable gain: $400

Losses can help balance your profits.

What Happens If You Don’t Report Crypto Tax?

Ignoring crypto tax can lead to:

- Fines

- Penalties

- Interest charges

- Legal action

Many governments now work with crypto exchanges to track transactions. Transparency is increasing every year.

It is always better to report honestly.

The Future of Crypto Tax

Crypto tax rules continue to evolve. Governments are introducing clearer regulations and stricter reporting requirements.

In the future, you can expect:

- More automated reporting from exchanges

- Better tracking systems

- Clearer global guidelines

- Stricter enforcement

As crypto becomes mainstream, tax compliance becomes more important.

Frequently Asked Questions (FAQs)

1. Do I pay crypto tax if I only buy and hold?

No. You usually pay crypto tax only when you sell, trade, or earn crypto income.

2. Is transferring crypto between wallets taxable?

No. Moving crypto between your own wallets is generally not taxable.

3. Do I pay crypto tax on gifts?

In many countries, the receiver does not pay tax immediately. However, selling the gift later may trigger capital gains tax.

4. How do tax authorities track crypto?

They work with exchanges and use blockchain analysis tools.

5. Can I avoid crypto tax?

Legally reducing crypto tax is possible. Avoiding it illegally can result in serious penalties.

6. Are NFTs taxed like crypto?

In many countries, yes. NFTs may be subject to similar capital gains rules.

7. Do I need special software for crypto tax?

It is not required, but software can make calculations easier.

Final Thoughts on Crypto Tax

Crypto tax may sound complicated at first. However, once you understand the basics, it becomes much easier to manage.

Remember these key points:

- Buying crypto alone is not taxable.

- Selling or trading crypto can trigger capital gains tax.

- Earning crypto counts as income.

- Good record-keeping is essential.

- Laws differ by country.

As cryptocurrency adoption grows, crypto tax compliance becomes more important. Staying informed helps you avoid penalties and protect your profits.

If you are serious about investing in digital assets, learning about crypto tax is just as important as choosing the right coin.

Take the time to track your transactions, understand your local rules, and report honestly. Doing so will give you peace of mind and keep your crypto journey smooth and successful.